CoreWeave is Undervalued

It's a lot of debt at first glance, but Nebius investors should understand the opportunity and valuation before dismissing the business.

Readers will know I’ve covered Nebius closely for the last year, and have secured returns of over 300 percent in the process (see here).

Valuing the business is tough, and a long-term, grounded view of the financials is something Wall Street is struggling to grasp. It is where my edge has come from in this stock. If you look out to 2028, the valuation looks a little rich. If you can extrapolate to 2030 and have a view on what the AI TAM will look like, the valuation is cheap.

Along the way, I’ve frequently compared Nebius to CoreWeave - the industry leader.

On revenue, CoreWeave is hugely ahead. On active power, CoreWeave is ahead. On management targets for 2030, CoreWeave is ahead. Yet I always saw more upside in Nebius, because Wall Street had a good grip on the CoreWeave story and the pricing was not that attractive.

Well, while Nebius is up roughly 150 percent year-to-date, CoreWeave is barely up 40 percent. While Nebius has made new highs throughout the year, CoreWeave is still more than 40 percent off its all-time high of $187.

CoreWeave’s market cap is $57 billion right now as I write. Nebius is also $57 billion. Yet CoreWeave is the neocloud leader, with the first-mover advantage and the Anthropic deal.

First principles would say this. If I believe Nebius is at an attractive valuation at a fraction of the revenue, and not the market leader, then CoreWeave quite simply has to be undervalued.

This article assesses if that is the case.

I am not going to cover the 2030 hypothesis or the AI TAM view here - I’ve done that elsewhere - see below.

My aim is to analyse why CoreWeave trades as it does, and whether the gap to fair value is real.

Contents:

CoreWeave - a quick primer

So why hasn’t the market rewarded CoreWeave?

The full comparison to Nebius

The valuation, and how the debt plays out

Base case and bull case

Conclusion

CoreWeave - a quick primer

For readers coming to this fresh.

What CoreWeave does:

Cloud infrastructure built purpose-specifically for AI workloads. Bare-metal compute, AI-native orchestration, inference services, and (via the Weights and Biases acquisition) developer-facing tooling.

49 active data centres at quarter-end. Over 1 GW of active power. 3.5 GW contracted. Targeting more than 8 GW by 2030.

IPO’d in March 2025 at $40. Currently $107.

Why it’s the leader:

$99.4 billion contracted revenue backlog as of 31 March 2026, up 284 percent year-on-year. That is twice the size of Nebius’s backlog.

Nine of the top ten AI model providers run on CoreWeave. The names: Microsoft, OpenAI, Anthropic, Meta, Mistral, IBM, Cohere, Nvidia and Google research. The one missing is Elon Musk’s xAI.

Customer concentration has improved meaningfully. In Q1 2026 the largest customer represented 45 percent of revenue, down from 72 percent a year earlier. The second-largest sat at 20 percent.

First cloud provider named NVIDIA Exemplar for inference on GB200 NVL72. NVIDIA closed a $2 billion equity investment in Q1 2026.

The Anthropic deal signed in April is genuinely meaningful. Especially when you consider my Anthropic at $1T in revenue thesis.

So why hasn’t the market rewarded CoreWeave?

In one word: debt.

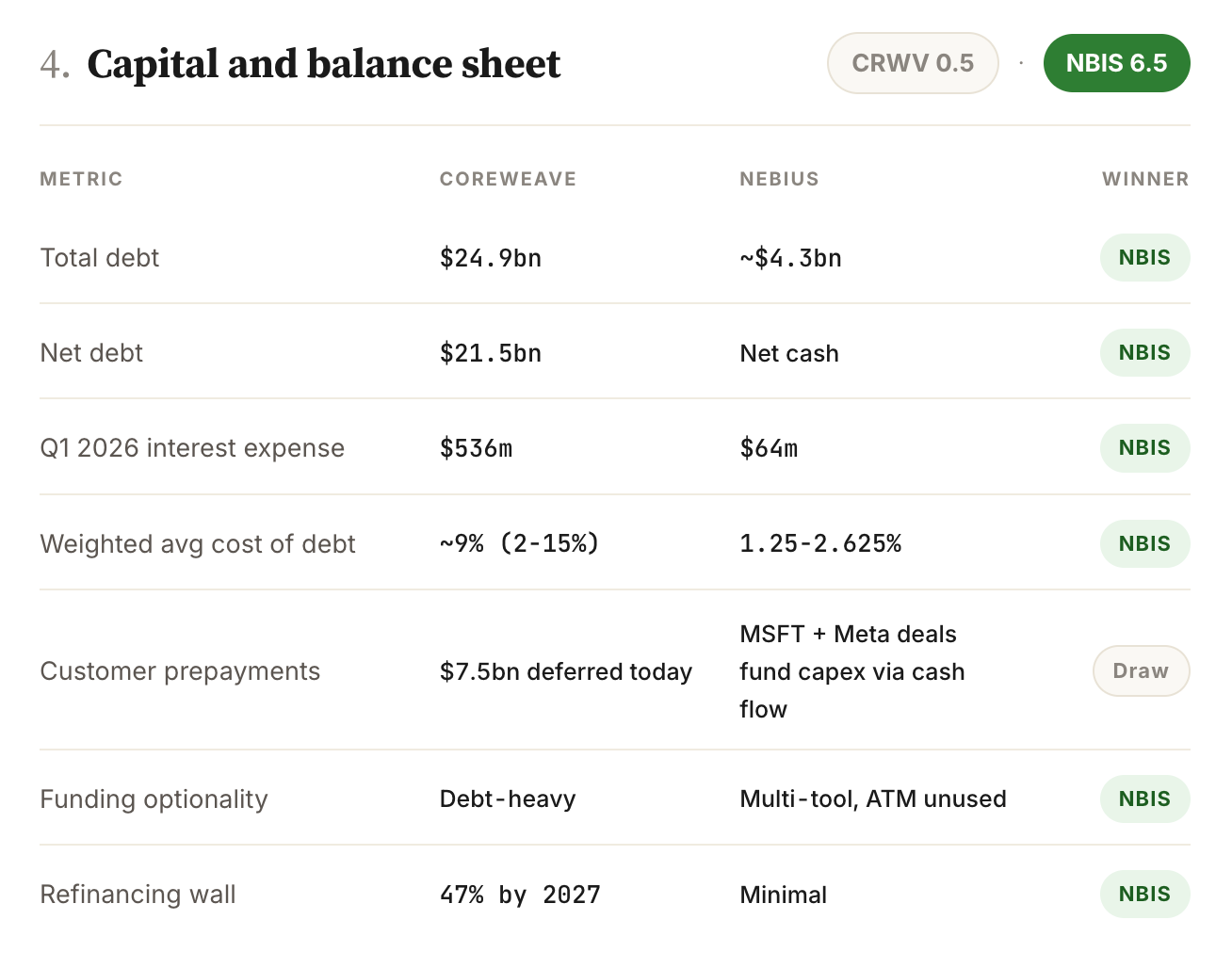

In a few more words… the market is worried about a credit cycle catching CoreWeave at the wrong moment. The company carries $24.9 billion of total debt, $10.1 billion of operating lease obligations, and net debt of roughly $21.5 billion. Q1 2026 interest expense alone was $536 million. Full-year 2026 interest expense is guided to $2.6 to $2.9 billion. These are genuinely staggering figures at first glance.

There is also a refinancing wall worth flagging: roughly 47 percent of CoreWeave’s debt principal - about $11.7 billion - matures by the end of 2027. The bears worry about what happens if credit markets are unfriendly at the moment that debt needs to roll.

Operating income in 2026 is guided to $900 million to $1.1 billion. Interest expense exceeds operating income by roughly three times.

That is the bear case in one number. The gap is funded by customer prepayments ($7.5 billion of deferred revenue on the balance sheet) and new debt issuance. The bear says: if either funding source dries up, CoreWeave is in big trouble.

I think the bears are right to flag this. I also think the bears are probably wrong about the conclusion.

Why I think the bears are wrong

A few things give me comfort, and I want to explain them at a high level.

1. The lenders have already seen CoreWeave at its worst.

In 2024, CoreWeave breached the terms on its $7.6 billion Blackstone-led loan facility because of administrative errors during European expansion. Blackstone waived the breaches without charging a fee, no payments were ever missed, and the same lender has since extended CoreWeave more credit on better terms.

2. The new debt is much cheaper than the old debt.

CoreWeave’s debt is a mix of older facilities at high rates and newer ones at much lower rates. The weighted average effective interest rate across the whole stack is roughly 9 percent today. The oldest and most expensive facility is at 15 percent. The newest facility - an $8.5 billion delayed draw term loan signed in Q1 2026 - is the first investment-grade-rated financing ever secured by AI infrastructure assets, with a blended effective rate of around 7 percent. As the older expensive debt rolls off and gets replaced with the newer cheaper debt, the average cost of borrowing keeps dropping.

3. CoreWeave’s creditworthiness is improving.

On 9 April 2026, S&P Global Ratings revised its outlook on CoreWeave from stable to positive, while affirming the B+ rating. The agency cited reduced customer concentration as a key driver. The rating itself is still sub-investment grade, but the direction is clearly positive.

4. The operating earnings are catching up fast.

CoreWeave is currently making roughly $1.16 billion of adjusted EBITDA per quarter. That is on track for around $5 billion annualised by the end of 2026. Against interest expense of $2.6-2.9 billion for the full year, that ratio is improving every quarter. By 2028, on management’s own trajectory, operating earnings should comfortably cover interest several times over. The current weakness is a 2026-2027 problem that resolves itself.

5. Customers are paying upfront, not just signing contracts.

CoreWeave has $7.5 billion of customer prepayments sitting on its balance sheet. That is real cash, paid in advance, before any service has been delivered. Microsoft, Meta, OpenAI and the AI labs are not just promising future revenue. They are funding the buildout directly.

6. The debt has not come at the cost of waves of equity dilution.

CoreWeave’s funding philosophy has clearly been debt-first, equity as a last resort. I will get into the detailed dilution comparison in section 4, but the headline is that CoreWeave has not had to issue waves of new shares to fund the buildout. Existing shareholders are taking on credit risk in exchange. Different risk, not no risk. But it is a defensible trade-off.

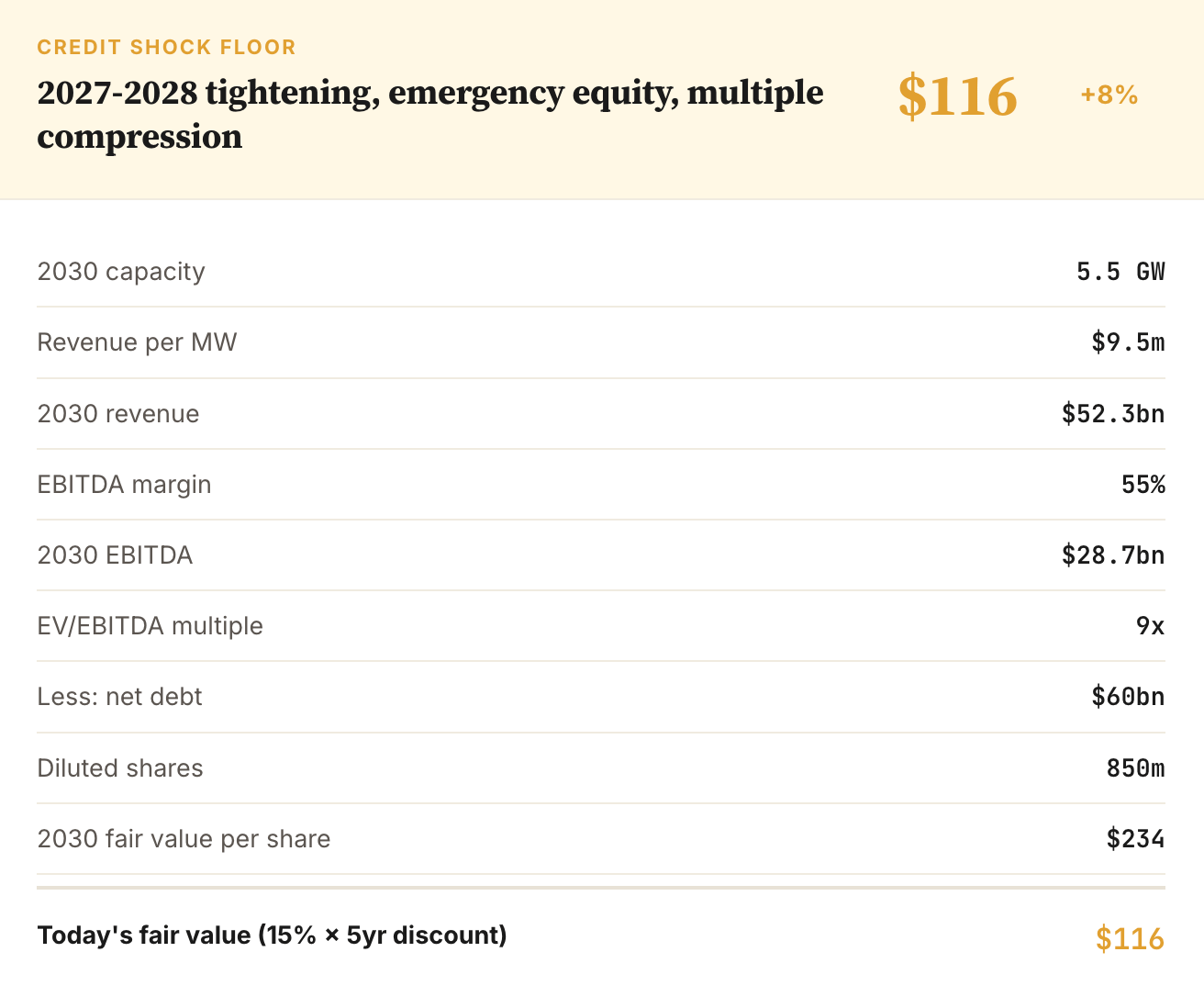

A basic credit stress scenario

To put a floor under the discussion, let me sketch what a bad outcome actually looks like. Assume that in 2027-2028 we get a serious tightening in credit markets - banks become reluctant to lend, interest rates rise sharply, and CoreWeave has to refinance its debt at much worse terms. In this world:

The build-out slows. CoreWeave reaches 5.5 GW of active power by 2030 instead of the 7 GW base case.

Refinancing happens at wider spreads. Net debt grows to $60 billion (from $50 billion in the base case).

Margins compress under operational stress. EBITDA margin lands at 55 percent instead of 58 percent.

CoreWeave is forced into emergency share issuance at depressed prices. The diluted share count reaches 850 million instead of 700 million.

The market keeps the multiple compressed because of the lingering credit overhang. 9x EV/EBITDA instead of 12x.

Working that through: 2030 fair value of $234, discounted back to today gives $116 per share.

The stock currently trades at $107. The market is essentially pricing the stress scenario as the central case.

That is the real observation worth sitting with. If you believe credit markets stay open, you are buying a company at a discount to fair value implied by a scenario most credit-market participants don’t think will happen.

And remember, in any of these scenarios, the operating profit covers the interest with room to spare by 2028-2029. The current weak coverage is a 2026-2027 problem that resolves itself as the contracted backlog converts into actual revenue.

The full comparison to Nebius

I want to be systematic about this rather than vibes-based. Five categories, multiple metrics in each, a point for the winner of each comparison. Final tally at the bottom.

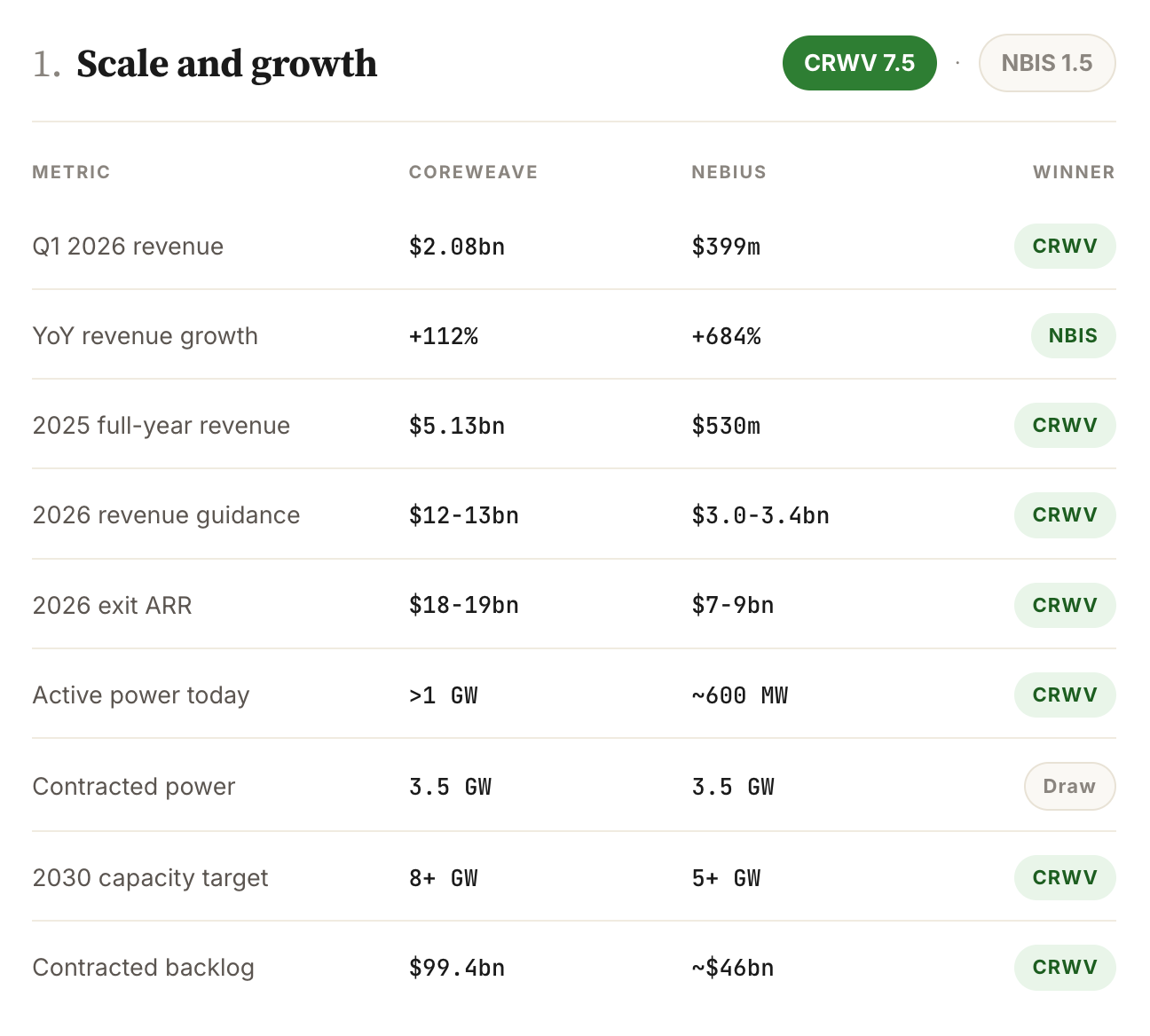

Scale and growth

Score: CoreWeave 7.5, Nebius 1.5. CoreWeave is the bigger, more developed operation today. Nebius is growing faster off a smaller base.

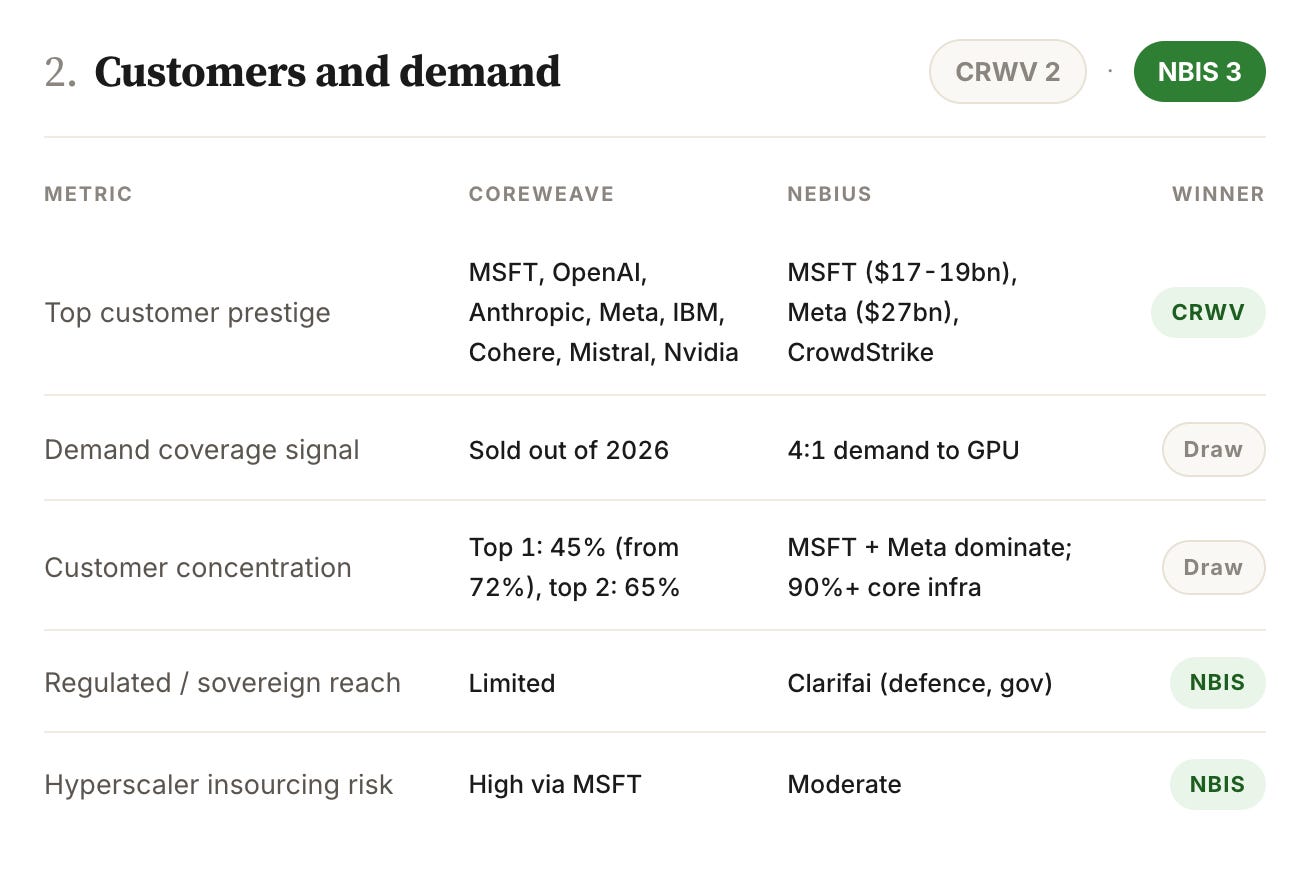

Customers and demand

Score: CoreWeave 2, Nebius 3. Both businesses are heavily concentrated - CoreWeave’s largest customer has come down from 72 to 45 percent of revenue, but Nebius is going the other way as the Microsoft and Meta deals ramp through 2026 and 2027. The honest read is that both have meaningful concentration risk.

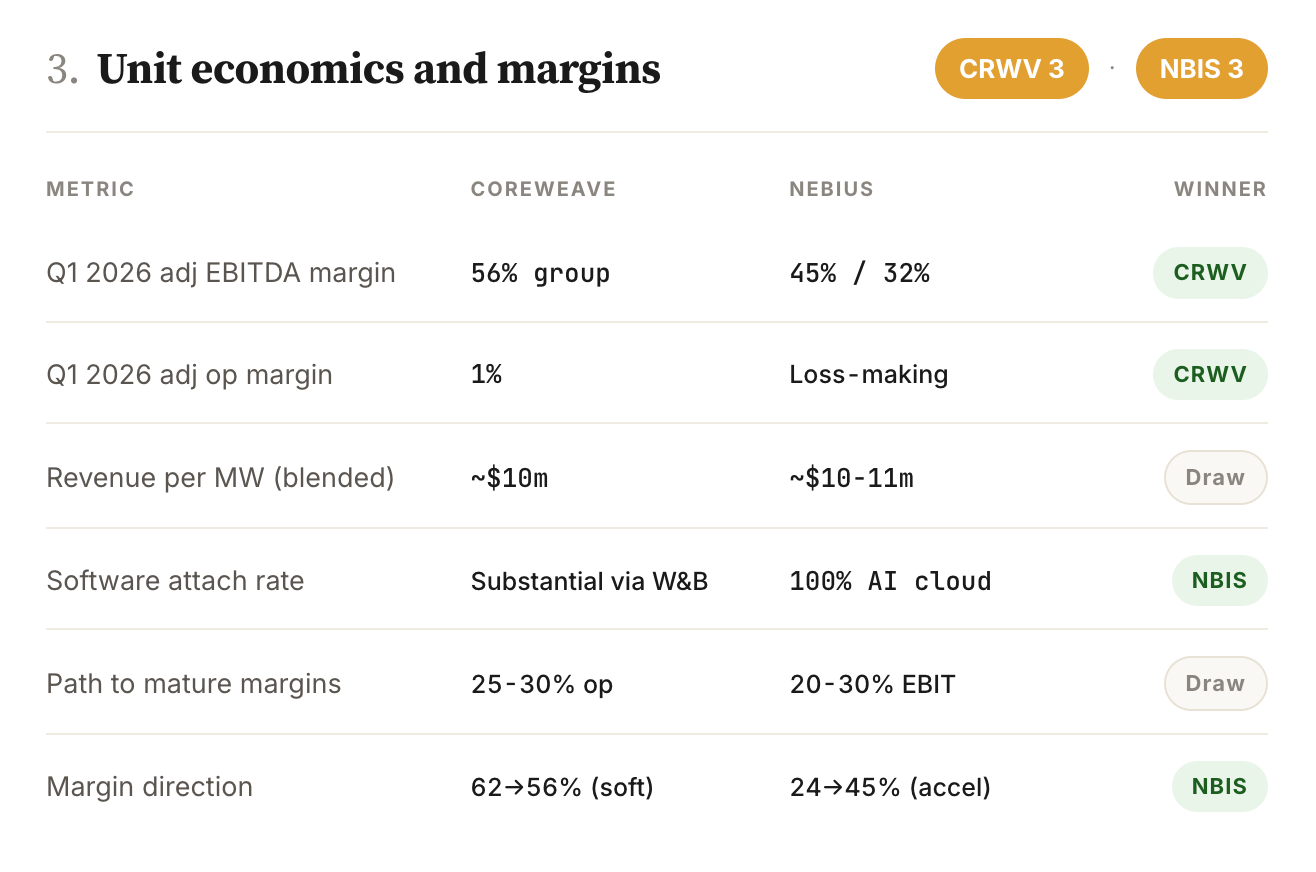

Unit economics and margins

Score: CoreWeave 3, Nebius 3. CoreWeave is two years ahead in absolute terms. But the direction favours Nebius - margins are accelerating, not decelerating.

Capital and balance sheet

Score: CoreWeave 0.5, Nebius 6.5. This is where the divergence is most extreme. Make no mistake - this is why CoreWeave trades at the discount it does.

Product and competitive positioning

Score: CoreWeave 2.5, Nebius 1.5. CoreWeave is NVIDIA’s deeper, longer-standing partner - joined NVIDIA’s cloud provider programme as Preferred Partner back in 2020, first to every chip generation since, and the only neocloud with both Exemplar status and a $6 billion-plus take-or-pay arrangement.

The overall scorecard

The scorecard is a tie at 15.5 each.

CoreWeave wins two categories outright (scale, product), Nebius wins two (customers, capital), and unit economics is a draw.

CoreWeave and Nebius are both businesses of high quality.

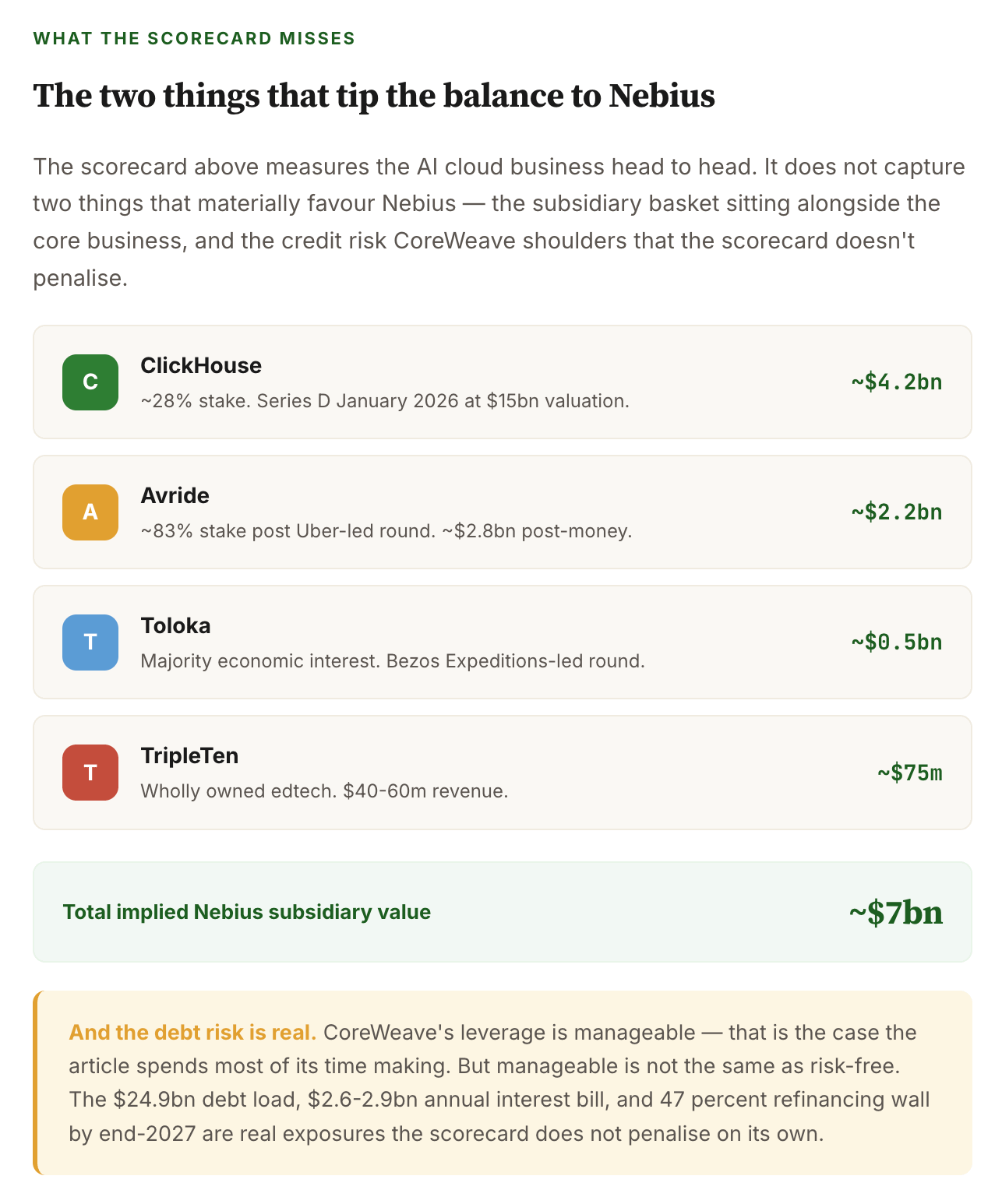

But the scorecard is not the whole story

Two things the scorecard does not capture, and both favour Nebius.

The subsidiaries. Nebius shareholders get a basket of non-core assets alongside the AI cloud business that have meaningful standalone value:

So while the scorecard ties on the measurable metrics, Nebius is still the better business once you include the subsidiaries and adjust for the credit risk the scorecard does not penalise.

What the scorecard does tell you, and tells you clearly, is that CoreWeave is much closer to Nebius on quality than the share prices suggest. And it is the price gap that this article is really about.

The valuation, and how the debt plays out